How a 3DS-enabled Payment Gateway Helps Reduce Chargebacks on Your eCommerce Business

Aditya Wibowo

April 2, 2024

5

minutes of read

Security is a cornerstone of any successful eCommerce operation. Among the most effective tools in the arsenal against fraud and chargebacks is 3D Secure (3DS) technology. If you've made a card payment online, it's likely you've encountered 3DS—even if you weren't aware of it. Let's delve into how 3DS works and its role in minimizing chargebacks.

Understanding 3DS in eCommerce Payments

3DS is a robust authentication protocol designed specifically for card payments. It hinges on a three-domain model encompassing the Acquirer Domain (merchant’s bank), the Issuer Domain (cardholder’s bank), and the Interoperability Domain (technology facilitating 3DS communication). This protocol is vital for both payment authentication and additional security checks, offering several ways to authenticate:

App-based Authentication: Integrated within a merchant's mobile app, this method prompts users for authentication during a transaction, often using biometric features like fingerprints for quick and secure verification.

Browser-based Authentication: Occurs on websites through a browser, where users are typically asked to enter a one-time password (OTP) sent via SMS or email, adding an extra layer of security to the transaction process.

3DS Requester Initiated: Designed for recurring payments or subscriptions, this approach verifies the cardholder’s information for scheduled transactions without requiring their active participation each time, streamlining the payment process for ongoing services.

The essence of 3DS is its requirement for consumers to authenticate their transactions, significantly reducing unauthorized payments and, consequently, chargebacks.

2DS vs 3DS Card Payments

While 2DS offers a simplified, two-domain model for authentication, 3DS presents a more comprehensive approach, including an additional security domain. The primary difference lies in the depth of security and the consumer's interaction with the authentication process, with 3DS requiring an OTP or similar verification method.

Considerations when Choosing Between 2DS and 3DS to Reduce Chargebacks

The choice between 2DS and 3DS impacts not just security but the overall customer experience. While both aim to secure transactions, 3DS stands out for its ability to prevent various forms of fraud, including 'friendly fraud'—where chargebacks are filed without legitimate grounds. Implementing 3DS can significantly enhance your efforts to mitigate such risks.

However, the effectiveness and preference for 3DS can vary globally. For instance, while some markets like the U.S. may still lean towards 2DS for its simplicity, others, like Singapore, have widely adopted 3DS, appreciating the added security layer of OTP verification. Knowing your target market's preferences is crucial to implementing the most effective payment security strategy.

Conclusion

Familiarity with 3DS and its application in a payment gateway can greatly benefit your eCommerce business by reducing chargebacks and enhancing transaction security. For those seeking a secure, robust payment gateway solution, Tazapay offers a comprehensive suite of features designed to protect your online transactions. Accredited by the Monetary Authority of Singapore (MAS) and equipped with PCI DSS certification, Tazapay ensures your business transactions are secure and trustworthy.

PayNow: Revolutionizing Singapore's Digital Payment System

In recent years, Singapore has rapidly evolved into a digital-first economy, with the island nation at the forefront of adopting innovative financial technologies. The emergence of digital wallets has signaled a shift in consumer preferences, with predictions suggesting they might soon eclipse traditional card payments. Central to this digital revolution is PayNow, a system that has transformed the way transactions are conducted in Singapore, promising a seamless, efficient, and secure method of payment.

What is PayNow?

Developed under the auspices of the Association of Banks in Singapore (ABS), PayNow is more than just a payment method; it's a cornerstone of Singapore's ambition to become a fully cashless society. This real-time payment platform enables users to send and receive money instantly using just a mobile number, NRIC/FIN, or UEN number, integrating seamlessly with the Singapore Quick Response Code (SGQR) for QR code payments. Supported by a consortium of major banks and financial institutions under the regulation of the Monetary Authority of Singapore (MAS), PayNow is a testament to Singapore's cohesive approach to financial innovation.

The Soaring Adoption of PayNow

Updating the statistics with the latest information, PayNow's trajectory in Singapore showcases the nation's accelerated embrace of digital payments. In 2020, Singapore witnessed a dramatic surge in real-time transaction volumes, reaching 138.38 million, a 48% increase from 2019. The value of these transactions also saw a significant jump of 40%, escalating from US$110 billion in 2019 to US$154 billion. The growth trend is projected to continue, with real-time transactions expected to climb at a compound annual growth rate (CAGR) of 23.2% to hit 392.94 million by 2025. This would elevate the total transaction value at a CAGR of 17.74%, underlining the increasing significance of digital payments in Singapore's financial landscape (Fintech Singapore).

The recent expansions into real-time cross-border payments further underline PayNow's evolving role in the financial ecosystem. 2023 marked a pivotal year as Singapore initiated real-time cross-border payment connections with neighboring countries. These developments, facilitated by the Monetary Authority of Singapore (MAS), aim to enhance convenience for cross-border fund transfers and small-value payments. The introduction of cross-border QR code payment linkages with Malaysia and Singapore, along with the establishment of a cross-border linkage between Singapore’s PayNow and India’s UPI, highlights the city-state's commitment to fostering financial inclusion and bolstering the ASEAN economy through improved payment connectivity (Fintech Singapore).

Unveiling the Benefits and Addressing the Drawbacks

Benefits

Real-time Payment Processing: The hallmark of PayNow is its ability to process payments in real-time. This immediacy is invaluable for both personal and business transactions, where speed can often be of the essence.

Universal Accessibility: PayNow's integration with a broad network of banks ensures that users can make payments across different financial institutions, breaking down the barriers traditionally associated with bank-specific platforms.

Stringent Security Measures: Security is paramount in digital transactions, and PayNow upholds the highest standards. Regulated by MAS, the platform employs robust security protocols, offering users peace of mind with each transaction.

Drawbacks

Technology Dependency: The reliance on smartphones and internet connectivity can be a limiting factor for some segments of the population, potentially excluding those without access to smart devices.

Privacy and Safety Risks: The convenience of using personal identifiers as payment addresses comes with potential privacy risks. There's also the ever-present threat of phishing and fraud, underscoring the need for constant vigilance.

Complicated Dispute Resolution: Navigating the process for resolving transaction disputes can be daunting, requiring engagement with recipients and financial institutions which can be time-consuming and frustrating.

Expanding Horizons: PayNow in International Transactions

While PayNow excels in facilitating local transactions, its integration with international payment systems like Tazapay represents a significant leap forward. This synergy allows Singaporean businesses and consumers to participate in the global marketplace more effectively, providing a streamlined process for cross-border transactions. Through platforms like Tazapay, users can easily transfer funds internationally, opening up new avenues for commerce and personal transactions alike.

Tazapay: A Closer Look

Tazapay stands out by offering a simplified and secure method for leveraging PayNow in international transactions. By facilitating the transfer of funds to Tazapay's Singapore account via PayNow, and then on to the recipient's foreign account, it bridges the gap between local and global payment ecosystems. This process not only enhances the utility of PayNow but also offers businesses a competitive edge in the international market.

Understanding the Financial Implications

The cost-effectiveness of PayNow for local transactions is clear, with nominal fees and a structure that promotes accessibility. However, the dynamics shift when considering international transactions. The use of third-party platforms like Tazapay introduces additional costs, albeit often lower than traditional banking fees. For businesses looking to expand globally, understanding these financial nuances is crucial in selecting the most efficient payment methods.

The Path Forward with PayNow

As PayNow continues to evolve, its potential to shape Singapore's digital economy grows ever more significant. Its integration with international payment gateways heralds a new era of financial connectivity, enabling Singapore to further solidify its position as a global financial hub. The ongoing developments in digital payment technologies promise to enhance PayNow's offerings, ensuring that Singapore remains at the forefront of the digital payment revolution.

For businesses and individuals alike, the journey towards a cashless society is filled with opportunities. Embracing platforms like PayNow and Tazapay not only facilitates easier transactions but also opens up new horizons for global engagement. As we look to the future, the role of digital payment systems in driving economic growth and fostering global connections cannot be underestimated.

In conclusion, PayNow's journey from a local payment solution to a key player in international transactions encapsulates the essence of Singapore's digital transformation. Its continued adoption and integration with global payment systems underscore the importance of digital innovation in today's interconnected world. As we embrace these technologies, the prospects for seamless, secure, and efficient transactions are boundless, heralding a new chapter in the story of digital payments.

Product Info

Local Payment Methods in India: How UPI Works In an International Payment Gateway

India stands at the forefront of the digital revolution, marking itself as one of the fastest-growing digital economies worldwide. With over 117 billion digital payment transactions recorded in 2023, and an average of 380 million transactions per day by December 2023, the country's trajectory towards digital integration is unmistakable. Central to this digital transformation is the Unified Payment Interface (UPI), developed by the National Payments Corporation of India (NPCI), embodying India's rapid embrace of digitalization to simplify financial transactions across the board.

UPI: The Cornerstone of Digital Payment in India

What Is UPI?

UPI stands as a beacon of innovation in real-time payment systems, facilitating inter-bank peer-to-peer (P2P) and peer-to-merchant transactions through a seamless two-click factor authentication process. Governed by the Reserve Bank of India (RBI), UPI's framework enables transactions via a smartphone application, heralding a new era of banking and financial services. Its resemblance to Singapore's PayNow underscores a global shift towards government-led digital payment solutions, fostering an ecosystem where transactions are not just secure but also universally accessible.

Embracing Digital Payments: User Trends and Preferences

In 2023, UPI transactions have seen remarkable growth, with the total transactions processed by UPI standing at 117.6 billion for the year. Specifically, for December 2023, UPI payments in India reached 12.02 billion transactions, with payments worth Rs 18.23 lakh crore being processed in just that month. This represents a 54% year-on-year growth in terms of volume and a 42% growth in transaction value annually (Economic Times) The adoption of UPI spans across diverse demographics, with its popularity not confined to urban centers but also penetrating rural areas, demonstrating the platform's wide acceptance and adaptability.

UPI's International Footprint: Bridging Global Transactions

International Payment with UPI:

The international operations of UPI have notably expanded beyond its initial reach. As of the latest updates in 2024, UPI's global footprint has extended to several new countries, making it a more versatile option for international payments. Specifically, France has recently adopted UPI, joining other countries like Bhutan, the United Arab Emirates (UAE), Malaysia, Singapore, Nepal, Oman, Qatar, Russia, Sri Lanka, Mauritius, and the United Kingdom in embracing this system. These expansions underscore UPI's growing acceptance and its potential as a global payment gateway.

This broadened adoption facilitates cross-border transactions, allowing users in these countries to leverage UPI for seamless and secure payments. The collaboration with various international partners and payment providers highlights UPI's versatility and its capability to streamline payment processes across different markets. This development is part of the National Payments Corporation of India's (NPCI) ongoing efforts to extend UPI's reach, reflecting the platform's potential to influence the global digital payment ecosystem significantly.

Cross-border Transactions with UPI: A Closer Look

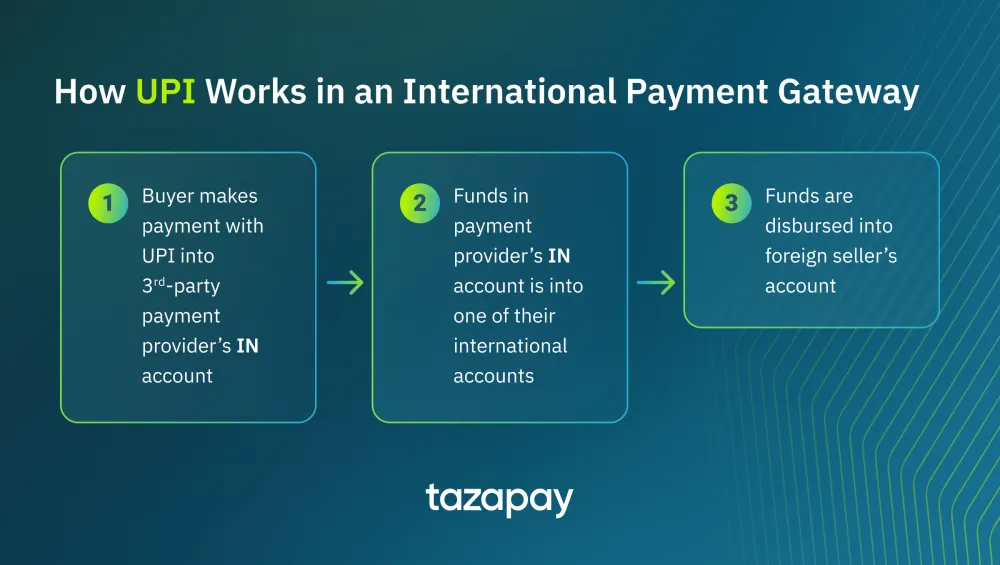

For regions yet to establish direct UPI connectivity, international transactions are streamlined through third-party payment providers, acting as bridges between UPI and global markets. Here’s how the process unfolds:

Initiating Payment: Users initiate transactions by transferring funds to the payment provider's bank account in India via UPI. This is typically done by scanning a QR code or barcode within the UPI app, representing the transaction amount.

Global Fund Transfer: Subsequently, these funds are transitioned into one of the payment provider’s international accounts. The final step sees the funds disbursed to the recipient's bank account abroad, completing the international transaction.

This model exemplifies UPI's adaptability and its growing acceptance as a versatile solution for international payments, providing a seamless, secure, and efficient transfer mechanism across different geographies.

Choosing the Right Payment Provider

Given the diverse landscape of third-party payment providers facilitating UPI transactions internationally, businesses and individuals are advised to select partners offering comprehensive support for a wide range of localized markets. This ensures not only the broad usability of UPI across various international platforms but also enhances the efficiency and security of cross-border payments.

With ongoing discussions to further expand UPI's reach to additional countries, the future of international digital payments looks promising, positioning UPI at the forefront of the global digital economy's evolution.

Analyzing UPI: Benefits and Challenges

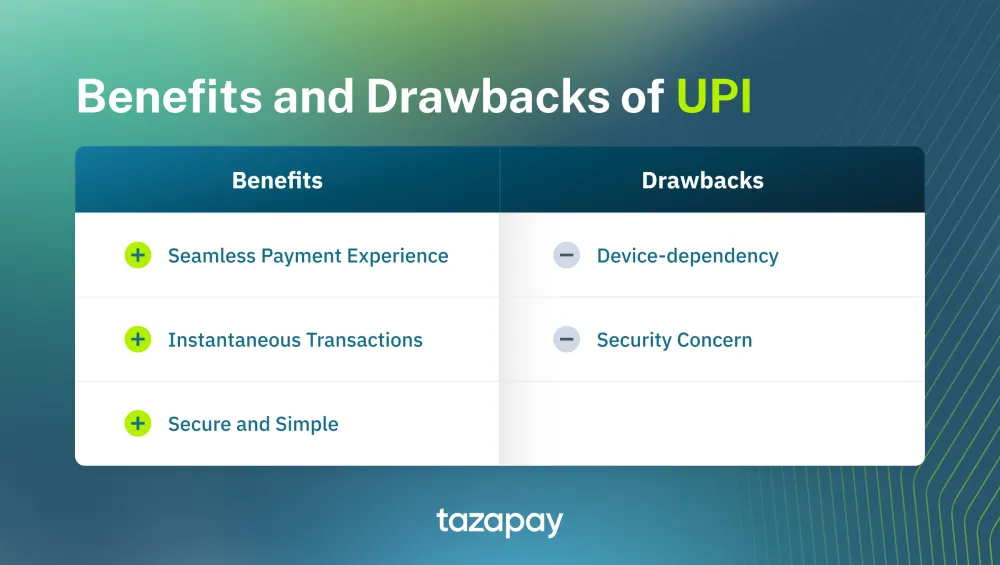

Benefits of UPI:

Seamless Payment Experience: UPI's integration with numerous payment apps and digital wallets, alongside its vast network of banks, provides a hassle-free transaction process.

Instant Transactions: The real-time processing capability of UPI ensures transactions are completed within seconds.

Security and Ease of Use: Enhanced with two-factor authentication and a unique UPI ID, the platform guarantees a secure yet straightforward payment experience.

Drawbacks of UPI:

Dependence on Internet Connectivity: The efficacy of UPI is contingent on reliable internet access, limiting its use in connectivity-challenged regions.

Security Concerns: Despite robust security measures, users must remain vigilant against potential phishing and fraud attempts due to the PIN-based authentication system.

UnderstandingTaxation and Compliance in UPI Transactions for International Businesses

Expanding into India's digital market requires a keen understanding of the country's tax and compliance landscape, especially for SaaS companies and digital eCommerce merchants leveraging UPI for transactions. Critical to this expansion is navigating the intricate documentation requirements, including obtaining a Tax Residency Certificate (TRC) and making a No Permanent Establishment (PE) Declaration, among others. These steps are vital for leveraging tax benefits under Double Taxation Avoidance Agreements (DTAAs) and ensuring smooth operation within the legal framework.

Furthermore, the implementation of GST on digital services and the significance of the Equalisation Levy on foreign e-commerce transactions underscore the evolving tax regime in India. These measures aim to ensure a level playing field between domestic and international players in the digital economy. As such, international businesses must stay abreast of these regulations to optimize their tax liabilities and maintain compliance. Download our eBook to understand this in detail

For businesses looking to streamline this process, leveraging platforms like Tazapay can provide significant advantages. Tazapay simplifies the complexities of tax collection, compliance, and remittance, enabling businesses to focus on growth and market penetration rather than administrative burdens.

Future Outlook: UPI’s Role in the Global Digital Economy and Tazapay’s Integration

As the Unified Payment Interface (UPI) continues to evolve, its influence is set to extend beyond the Indian market, marking a significant shift in the global digital payment ecosystem. UPI’s initiatives aimed at expanding its international reach and enhancing its features for global usability are pivotal. In this landscape of growth and innovation, UPI is well-positioned to facilitate seamless and secure online payments on a worldwide scale, embodying India's ambitious vision for a digitally empowered global economy.

In this evolving scenario, Tazapay stands out as a crucial player, offering an innovative solution that integrates UPI alongside other local payment options across 80+ locations with just one integration. This strategic collaboration enables businesses to leverage UPI’s simplicity and security while also accessing a broad spectrum of payment methods globally, ensuring they can meet the diverse preferences of customers worldwide. Tazapay's one-stop payment solution signifies a leap towards creating a more inclusive and accessible digital payment infrastructure, making it easier for businesses to engage in cross-border commerce without the hassle of managing multiple payment integrations or local entities.

Expanding Your Reach: Why Dragonpay is Essential for Philippine Cross-Border Sales

Introduction

The digital landscape in the Philippines is undergoing a remarkable transformation, marked by a surge in e-commerce and digital payments. This evolution presents a golden opportunity for international businesses looking to expand their footprint in Southeast Asia. With the Philippines at the forefront of digital adoption, the market's potential for cross-border commerce is immense. Enter Dragonpay, a payment solution that is revolutionising how businesses access this vibrant and diverse market.

The Digital Commerce Opportunity in the Philippines

The Philippines is witnessing an e-commerce revolution, with growth rates outpacing many of its regional counterparts. A robust digital infrastructure, coupled with one of the world's highest social media usage rates, has created a fertile ground for digital commerce. This is further bolstered by a young, tech-savvy population that is increasingly inclined towards online shopping. The result? A growing e-commerce market ripe for international sellers.

Statistics underscore this potential: with internet penetration exceeding 70% and a digital payment adoption rate of 92%, the Philippines is not just a market—it's an opportunity. The country's e-commerce sector is expected to reach USD 29.57 billion by 2029, signaling a lucrative avenue for businesses aiming to tap into Southeast Asia. (https://www.mordorintelligence.com/industry-reports/philippines-ecommerce-market#:~:text=Philippines%20E%2Dcommerce%20Market%20Analysis,period%20(2024%2D2029).

Understanding Dragonpay

What Is Dragonpay?

Dragonpay is not just a payment platform; it's a bridge between the traditional and the digital, the local and the international. Founded to address the Philippines' unique market challenges, Dragonpay offers a plethora of payment solutions that cater to a wide array of consumers, including the significant unbanked population. By providing options beyond traditional banking, such as over-the-counter payments and online banking transfers, Dragonpay has become an integral part of the Philippine e-commerce ecosystem.

How Dragonpay Supports Cross-Border Transactions

For international merchants, Dragonpay is a gateway to the Philippine market. It simplifies the complex landscape of local payments, enabling businesses to accept payments through methods preferred by Filipino consumers. This capability is crucial for cross-border transactions, where familiarity and trust in payment methods significantly influence consumer behaviour.

Advantages of Using Dragonpay for International Sellers

Dragonpay offers several compelling advantages for international businesses:

Ease of Transaction: Simplify the checkout process for your customers by offering payment options they know and trust.

Access to a Broader Customer Base: Tap into the significant segment of the Filipino population that is either unbanked or prefers non-traditional banking solutions.

Secure Payment Processing: Benefit from a platform that adheres to strict security standards, minimizing the risk of fraud and ensuring customer trust.

Success stories abound, from small online retailers who have expanded their market reach to multinational corporations that have streamlined their payment processes in the Philippines. These narratives underscore Dragonpay's role in enabling businesses to flourish in the Philippine digital marketplace.

How Dragonpay Works for International Transactions

The Process Explained

For businesses seeking to leverage Dragonpay for cross-border sales, understanding the transaction process is crucial. Here's a breakdown of how Dragonpay works in conjunction with a payment gateway like Tazapay to enable international transactions:

Making the Payment: When a buyer in the Philippines decides to make a purchase from an international seller, they select Dragonpay as their payment option at checkout. The transaction is initiated through Tazapay, which acts as the bridge between Dragonpay and the seller, ensuring the payment process adheres to both local and international payment standards.

Funds Transfer: Once the payment is completed via Dragonpay, the funds are initially collected in Tazapay's Philippine account. This local collection is a critical step, allowing for the seamless processing of payments made using various methods available through Dragonpay, from online banking to over-the-counter deposits.

Disbursing to the Seller: After the funds are securely held in the Philippine account, Tazapay then transfers these to one of its international accounts. This step is where the cross-border element comes into play, facilitating the movement of funds across borders without the need for the seller to manage multiple local accounts. Finally, the funds are disbursed into the foreign seller's account, completing the transaction.

This streamlined process simplifies the complexity of international payments, making it easier for sellers to access the Philippine market without navigating the intricacies of local banking and payment systems. By leveraging the capabilities of Dragonpay through a comprehensive payment gateway like Tazapay, businesses can ensure a smooth, secure, and efficient transaction process for both themselves and their customers.

Step-by-Step: Integrating Dragonpay into Your Business through Tazapay

Integrating Dragonpay as a payment option for your business requires partnering with a comprehensive payment gateway like Tazapay. Tazapay simplifies the process, enabling access not only to Dragonpay but also to a wide array of local payment options across more than 80 countries with a single integration. Here's how to get started:

Sign Up: Register your business with Tazapay. This initial step is your gateway to accessing Dragonpay along with numerous other local payment methods globally.

Complete KYB: As part of the onboarding process, you'll need to complete the Know Your Business(KYB) requirements. This step is essential for ensuring compliance and security for your transactions across borders.

Integrate: Choose the best integration option that suits your business needs. Tazapay offers various integration methods, including APIs, plugins, hosted checkout solutions, and white-label solutions. These flexible options ensure that you can offer Dragonpay and other payment methods seamlessly on your platform, providing a tailored and localized checkout experience for your customers.

Start Collecting via Dragonpay: Once integration is complete and you go live, you can start collecting payments through Dragonpay. This allows your business to tap into the Philippine market effectively, offering customers their preferred payment method and enhancing their shopping experience.

Tazapay's dedicated support team is available to guide you through each step, from sign-up to integration, ensuring a smooth and efficient setup process. By choosing Tazapay as your payment gateway, you not only gain access to Dragonpay but also unlock the potential to expand your business reach globally, catering to a diverse customer base with localized payment options.

Navigating Challenges in Cross-Border Sales with Dragonpay

Cross-border sales come with their set of challenges, from navigating local payment preferences to addressing security concerns. Dragonpay is designed to mitigate these challenges by:

Providing a familiar payment interface for Filipino consumers, thus increasing conversion rates.

Offering robust fraud detection and prevention mechanisms to safeguard transactions.

Ensuring compliance with local regulations, reducing the administrative burden on merchants.

Preparing for the Future: Trends in Cross-Border E-Commerce

The landscape of cross-border e-commerce is constantly evolving. Emerging trends indicate a shift towards more personalized and secure online shopping experiences. Dragonpay stays ahead of these trends by continuously updating its platform with features that enhance user experience and security, ensuring businesses remain competitive in the dynamic Philippine e-commerce market.

Conclusion

Dragonpay is more than a payment gateway; it's a strategic tool for businesses aiming to capitalize on the Philippine e-commerce boom. Its comprehensive suite of services not only facilitates access to this lucrative market but also positions businesses for success in the global e-commerce arena.

Tazapay Pte. Ltd. (UEN: 202010604W) is licensed by the Monetary Authority of Singapore (MAS) as a Major Payment Institution (Licence No. PS20200638), authorizing a broad range of payment services including cross-border transactions. Licence details.

Tazapay Canada Corp. (Incorporation number: BC1313641) is regulated by the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) as a Money Services Business (MSB registration number M21439799), ensuring compliance with Canadian financial regulations. Registration information.