Sofort was a bank transfer payment method available across Germany, Austria, Switzerland, Belgium, and the Netherlands. Klarna acquired Sofort in 2014 and, in late 2023, announced its consolidation into Klarna Pay Now. The standalone Sofort payment method was fully discontinued on September 30, 2024 [1].

Merchants that relied on Sofort needed to migrate to Klarna Pay Now (which provides similar bank transfer functionality under the Klarna brand) or switch to alternative bank transfer methods such as SEPA Instant, Open Banking-based payment initiation, or country-specific methods like iDEAL or EPS.

This is not an isolated event. Giropay, Germany's other major bank transfer method, was also deprecated in mid-2024. The European payment landscape is consolidating around SEPA Instant as the universal A2A rail, with country-specific methods serving particular markets.

SEPA Instant Credit Transfer (SCT Inst) is the most important development in European payments since the original SEPA standardization. It settles transfers in under 10 seconds, 24 hours a day, 365 days a year, at fees no higher than standard SEPA transfers [2].

Since January 2025, Eurozone banks are required to offer SEPA Instant for receiving payments. The sending obligation follows later. Non-eurozone EU member states must comply by January 2027 (receiving) and July 2027 (sending plus Verification of Payee) [2].

Verification of Payee (VoP) is now mandatory alongside SEPA Instant in the Eurozone. Before a payment is executed, the sending bank verifies that the payee name matches the IBAN. This reduces fraud and misdirected payments but adds a verification step that merchants and platforms need to account for in their checkout flows.

SEPA Instant will progressively replace standard SEPA Credit Transfers for most use cases. For businesses collecting payments from European customers, SEPA Instant provides immediate payment confirmation with irrevocable settlement, significantly better than the 1-2 day settlement window of standard SEPA.

While SEPA Instant provides a universal rail, several country-specific payment methods retain dominant positions in their home markets. These methods predate SEPA Instant and continue to be preferred by local consumers due to familiarity, integration with domestic banking apps, and established merchant acceptance.

iDEAL (Netherlands): The dominant online payment method in the Netherlands, historically accounting for around 70% of Dutch e-commerce transactions. iDEAL redirects the customer to their bank's online banking portal to authorize a direct transfer. For any business selling to Dutch consumers, iDEAL is non-negotiable. iDEAL is transitioning to iDEAL 2.0, which builds on SEPA Instant and Open Banking infrastructure.

Bancontact (Belgium): Belgium's domestic debit card and online payment scheme, used by the majority of Belgian consumers for both in-store and online purchases. Bancontact supports card-present (contactless NFC) and card-not-present (online redirect) transactions. Its integration with Payconiq enables QR-based mobile payments.

EPS (Austria): Austria's online bank transfer method, which redirects customers to their Austrian bank for payment authorization. Similar to iDEAL in function, EPS is the preferred online payment method for Austrian consumers alongside cards.

Klarna Pay Now: The successor to Sofort. Klarna Pay Now provides immediate bank transfer functionality under the Klarna brand. It is available across Germany, Austria, the Netherlands, and other European markets where Sofort previously operated. Klarna also offers Pay Later (invoice) and installment options, though those are separate products.

Przelewy24 (Poland): Poland's dominant online payment aggregator, connecting to all major Polish banks. Essential for any business selling into the Polish market.

For international businesses already selling into Europe via card networks, the EU's Interchange Fee Regulation (IFR) creates a structurally different cost environment than the US or APAC.

Consumer card interchange in the EU is capped at 0.2% for debit and 0.3% for credit [3]. Compare this to the US, where interchange ranges from 1.0-2.5% depending on card type and is uncapped. A transaction that costs a merchant 2.5% in interchange in the US costs 0.2-0.3% in the EU.

Cross-border card-not-present interchange within the EEA is capped at 1.15% for debit and 1.50% for credit [3]. Post-Brexit UK ↔ EEA interchange is higher and under regulatory review. For a detailed breakdown of all five cost layers in payment gateway pricing, including how EU caps compare to uncapped markets, see our gateway costs blog.

The practical implication: card acceptance in Europe is significantly cheaper than in the US, which changes the calculus on whether APMs save money. In Europe, the case for APMs is less about cost saving and more about conversion optimization. iDEAL in the Netherlands and Bancontact in Belgium convert at higher rates than international cards because they are the methods consumers expect and trust.

Three priorities for European payment acceptance.

First, ensure SEPA Instant readiness. As VoP becomes mandatory across the Eurozone, your payment infrastructure needs to support the verification step. SEPA Instant provides immediate, irrevocable settlement, which eliminates the cash flow uncertainty of standard SEPA transfers.

Second, integrate country-specific APMs for your top European markets. iDEAL for the Netherlands, Bancontact for Belgium, EPS for Austria, Przelewy24 for Poland. These methods can lift checkout conversion by 10-20% over cards alone because they are the payment methods local consumers prefer [4].

Third, take advantage of EU interchange caps. If you are selling into Europe from outside the EU, your card processing costs are structurally lower than in the US or APAC. A payment gateway with local European acquiring can further reduce costs by processing transactions as intra-EEA rather than cross-border.

For the equivalent breakdown of how e-wallets and QR payments work across Southeast Asia, where the payment landscape is structurally different from Europe, see our SEA payments guide.

[1] Solidgate. "Klarna Deprecated Sofort: What Merchants Need to Do." May 2026. https://solidgate.com/blog/klarna-deprecated-sofort-as-a-payment-method/

[2] Klarna. "How Instant Payments Will Spark Competition in Europe." 2023. https://www.klarna.com/international/press/klarna-comment-how-instant-payments-will-spark-competition-in-europe/

[3] Adyen. "Interchange Fees Explained." April 2026. https://www.adyen.com/knowledge-hub/interchange-fees-explained

[4] GR4VY. "Payment Methods by Country 2026: What Dominates Each Market." April 2026. https://gr4vy.com/posts/payment-methods-by-country-2026-what-dominates-each-market-and-how-to-accept-them/

Thailand is one of Southeast Asia’s fastest-growing digital economies. With a population that is increasingly mobile-first, digital payments are now part of everyday life. For international businesses selling to Thai customers, however, the biggest challenge remains checkout success.

Credit and debit cards remain important, but they often fall short. Many transactions are declined, card coverage is limited outside urban centers, and foreign exchange costs can discourage buyers. This results in abandoned checkouts and lost revenue opportunities.

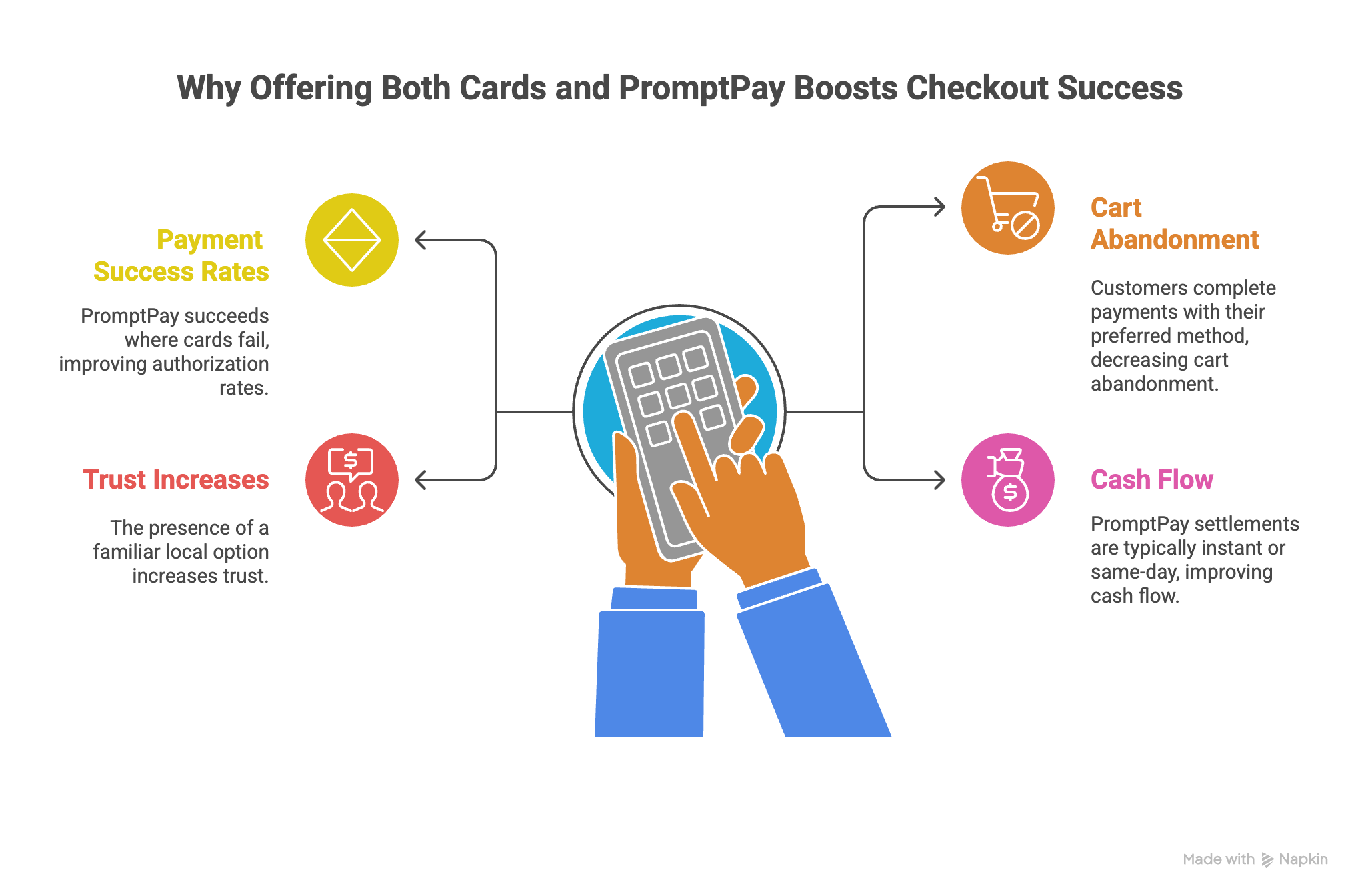

PromptPay, Thailand’s national QR-based payment method overseen by the Bank of Thailand and National ITMX, has become the mainstream alternative. With more than 81 million registrations and billions of transactions every month, it is trusted by consumers across all sectors.

For global B2B and e-commerce businesses, enabling PromptPay alongside cards means fewer failed payments, higher authorization rates, and greater customer trust.

With Tazapay, you can offer PromptPay through a unified checkout that also supports cards and 80+ other local payment methods, going live within days.

PromptPay adoption has grown dramatically, making it an indispensable part of Thailand’s payment ecosystem:

This progression shows PromptPay’s journey from a domestic initiative to a critical tool for international businesses. Offering PromptPay at checkout has become an expectation, not a differentiator, for global merchants operating in Thailand.

.png)

E-commerce platforms and online marketplaces often see high cart abandonment in Thailand due to card failures or customer hesitation.

By offering PromptPay alongside cards:

PromptPay has become a default option for Thai shoppers, so businesses that include it maximize completed orders and revenue.

Thailand’s travel industry is huge, and online booking platforms often face failed transactions at checkout. This is particularly challenging for mid-range purchases like hotel reservations or tour bookings.

PromptPay helps by:

For online travel agencies and hotel platforms, PromptPay improves booking completion and reduces drop-offs.

Thailand has one of Asia’s most engaged digital populations, with significant spending on gaming and online products. But micro-transactions and one-off purchases often fail on card-only checkouts.

PromptPay ensures:

This makes PromptPay especially valuable for digital platforms, app stores, and gaming companies serving Thai customers.

As online education grows in Thailand, payment access remains a barrier. Many students and professionals lack international-ready cards, making it difficult to enroll in global courses.

PromptPay solves this by:

Businesses that provide multiple payment options serve more customers and reduce payment risk. In Thailand:

PromptPay complements cards rather than replacing them. Together, they capture the widest possible customer base and maximize checkout success.

Merchants relying only on cards or international transfers face:

Adding PromptPay addresses these risks and future-proofs your checkout strategy.

Tazapay simplifies the complexity of enabling PromptPay for cross-border businesses:

Whether you prioritize speed or brand control, Tazapay gives you the flexibility to add PromptPay and optimize checkout for higher authorization rates and faster settlement.

Thailand’s digital economy offers huge opportunities for global businesses, but only if they solve checkout friction. Cards remain necessary, but PromptPay has become an equally important option.

With more than 81 million registrations and over 2 billion monthly transactions in 2025, PromptPay is one of Thailand’s most trusted and widely used payment methods. Businesses that offer it alongside cards increase conversions, reduce abandonment, and build stronger customer trust.

With Tazapay, you can integrate PromptPay quickly and compliantly, enabling a better checkout experience for your Thai customers.

Ready to start? Talk to Tazapay and enable PromptPay today.

The Australian e-commerce market continues to show significant growth. In 2024, the market is projected to reach a revenue figure of $35.92 billion. This represents a continuation of the rapid growth seen in previous years, fueled by various factors including the increasing preference for online shopping among Australian households and the rise of digital payment solutions like POLi. Additionally, the Australian eCommerce market is expected to grow at a compound annual growth rate (CAGR) of 8.33%, reaching $49.47 billion in sales by 2028.

The Rise of POLi in Australian E-commerce

POLi has carved a niche as one of the most preferred online payment options in Australia, facilitating seamless Pay Anyone internet banking payments. Its integration with Australia Post’s robust infrastructure lends it unparalleled reliability and trust, making it a cornerstone of the digital payments landscape in the region.

How POLi Works

At its core, POLi enables users to conduct direct funds transfers from their bank accounts to merchants without the need for credit cards. This simplicity of use, coupled with the elimination of the need for a traditional account registration process, positions POLi as a user-friendly payment gateway for Australians and international merchants alike.

Instantaneous Transactions

POLi Payments are distinguished for their rapid processing, where transactions, particularly through POLi PayID, are completed almost instantly. This efficiency is paramount for businesses that prioritise quick turnaround times and for consumers who value speed in their online transactions.

Security Assured

With regular security reviews and the use of 2048-bit encrypted SSL certificates, POLi assures the utmost privacy and security for its users. Sensitive information, such as usernames and passwords, are never stored, providing a safe transaction environment.

No Registration Needed

POLi simplifies the online payment process by eliminating the need for account registration. Users can select POLi at checkout, facilitating a smoother and faster transaction process, enhancing the overall user experience.

Facilitating Cross-Border Payments

For international merchants eyeing the Australian market, POLi serves as an essential bridge, enabling direct payments from any Australian bank. This multi-bank redirect capability ensures merchants can offer a localized payment solution, essential for tapping into Australia's lucrative e-commerce sector.

The Checkout Process with POLi

Within Australia and New Zealand:

For International Transactions:

Region-locked

One of the primary drawbacks of POLi is its availability, which is currently limited to Australia and New Zealand. This regional exclusivity can pose challenges for international transactions, necessitating a third-party payment provider for global merchants.

Internet Reliant

Given Australia's vast landscape and varied internet connectivity, the online nature of POLi Payments means that transactions may sometimes be hindered by network stability issues, affecting the consistency of the payment experience.

POLi endeavors to keep costs low, charging a modest 1.25% per transaction, capped at 3%, and a flat fee of AUD 0.95 for PayID payments. While third-party payment providers may introduce additional costs, the overall affordability of POLi transactions remains a significant advantage for businesses and consumers.

Market Penetration Strategies

Adopting POLi can dramatically enhance an international merchant's appeal to Australian consumers, offering a familiar and trusted payment method. This localization strategy not only boosts sales but also builds consumer trust and loyalty.

Enhancing Customer Experience with POLi

Integrating POLi into your payment options can significantly streamline the checkout process, reducing cart abandonment rates and elevating the overall shopping experience. The convenience and security of POLi payments encourage repeat business, fostering a loyal customer base.

In Australia's dynamic e-commerce environment, POLi Payments emerges as a pivotal solution for businesses aiming to capitalize on digital market opportunities. Its integration into international payment gateways offers a seamless, secure, and user-friendly transaction process, vital for tapping into Australia's growing online consumer base.

Ready to Embrace the Future of Payments?

Exploring POLi as part of your payment solutions is more than just offering another payment method; it's about unlocking the full potential of the Australian e-commerce market. For international merchants, the journey towards maximizing e-commerce success in Australia starts with understanding and implementing localized payment methods like POLi. Discover how integrating POLi Payments can transform your business and contact Tazapay for seamless international transactions today.

Familiarising yourself with financial institutions in Singapore is crucial for the successful localization of your business. As one of the most dynamic financial hubs in Asia, Singapore offers a fertile ground for expanding your eCommerce business.

Read on for a full guide to 10 of the top banks in Singapore that are pivotal for your online payment gateway, and a quick overview of the payment landscape in the country.

The banking infrastructure in Singapore is not only steadily optimised for an increasingly digitised global economy but also well-integrated into the local populace. In 2022, Singapore topped the area of financial inclusion, beating powerhouse economies such as the United States, Britain, Hong Kong and Japan1, and attained a 92% internet penetration level in the country.2

This digital transformation is further supported by the government's proactive stance towards digitalisation, with initiatives such as PayNow and e-wallet integration enhancing Singapore's online payment gateway capabilities.

As such, the payments landscape in Singapore is largely digital, with card payments being the most popular online payment method. However, current trends in local payment solutions forecast that e-wallet payments will soon surpass cards by 2026, signalling a significant shift in consumer preferences.3

DBS Bank, the largest bank in Singapore by total assets (SGD 686 billion as of 2021), was founded in 1968 by the government of Singapore. The bank excels in providing a variety of financial products and services, including personal and business banking, investment banking, and wealth management. DBS Group champions electronic payment methods for its customers:

Most third-party international payment gateways, including Tazapay, support DBS's bank redirected payment methods and card payments, catering to eCommerce transactions. Incorporating the PayNow system enhances familiarity for Singaporean buyers, fostering trust for international merchants.

Founded in 1932, OCBC is the second-largest bank in Singapore with over SGD 542 billion in total assets as of 2020. It provides robust financial products and services suitable for a thriving digital economy:

UOB, ranking third in Singapore by assets with over SGD 459 billion (2021), has a prominent presence in the region, headquartered in the former tallest building in Southeast Asia. The bank offers:

A multinational presence since 1859, Standard Chartered Bank boasts over SGD 153 billion in total assets as of 2021 and is a trusted name among Singaporeans due to its long-standing reliability. The bank offers:

Maybank, a leading Southeast Asian bank with a strong Singapore presence (SGD 69 billion in assets as of 2021), operates over 2,600 branches across 18 countries. The bank offers:

Citibank, with SGD 52 billion in assets as of 2021, offers a diverse range of financial services, reinforcing its significant role in Singapore's banking sector. The bank offers:

HSBC, a global financial institution, holds approximately SGD 27 billion in assets as of 2021 and shares a historical lineage with Standard Chartered in British colonial history. The bank offers:

With a robust SGD 5.2 billion in assets (2021), the Bank of China marks China’s expanding influence in the Asian digital economy. The bank offers:

This Japanese banking leader, significant in Singapore, manages over SGD 5.2 billion in assets (2021) and has been a solid player since 1963. The bank offers:

Europe's largest banking group, BNP Paribas, holds about 3.7 billion SGD in total assets (2021) and maintains a strong European and global banking footprint. The bank offers:

With a clear understanding of the preferred banks in Singapore, you can better tailor your online business for the local market. Integrating with these banks through a payment gateway like Tazapay not only sets your business apart but also leverages localised payment methods to enhance customer trust.

Tazapay, operating with a 0.8%-2.5% fee for international transactions through local bank transfers, offers a compelling advantage for expanding your business in Singapore. Contact Tazapay today for more details and to take your business to the next level.

Sources

The digital landscape in the Philippines is undergoing a remarkable transformation, marked by a surge in e-commerce and digital payments. This evolution presents a golden opportunity for international businesses looking to expand their footprint in Southeast Asia. With the Philippines at the forefront of digital adoption, the market's potential for cross-border commerce is immense. Enter Dragonpay, a payment solution that is revolutionising how businesses access this vibrant and diverse market.

The Philippines is witnessing an e-commerce revolution, with growth rates outpacing many of its regional counterparts. A robust digital infrastructure, coupled with one of the world's highest social media usage rates, has created a fertile ground for digital commerce. This is further bolstered by a young, tech-savvy population that is increasingly inclined towards online shopping. The result? A growing e-commerce market ripe for international sellers.

Statistics underscore this potential: with internet penetration exceeding 70% and a digital payment adoption rate of 92%, the Philippines is not just a market—it's an opportunity. The country's e-commerce sector is expected to reach USD 29.57 billion by 2029, signaling a lucrative avenue for businesses aiming to tap into Southeast Asia. (https://www.mordorintelligence.com/industry-reports/philippines-ecommerce-market#:~:text=Philippines%20E%2Dcommerce%20Market%20Analysis,period%20(2024%2D2029).

Dragonpay is not just a payment platform; it's a bridge between the traditional and the digital, the local and the international. Founded to address the Philippines' unique market challenges, Dragonpay offers a plethora of payment solutions that cater to a wide array of consumers, including the significant unbanked population. By providing options beyond traditional banking, such as over-the-counter payments and online banking transfers, Dragonpay has become an integral part of the Philippine e-commerce ecosystem.

For international merchants, Dragonpay is a gateway to the Philippine market. It simplifies the complex landscape of local payments, enabling businesses to accept payments through methods preferred by Filipino consumers. This capability is crucial for cross-border transactions, where familiarity and trust in payment methods significantly influence consumer behaviour.

Dragonpay offers several compelling advantages for international businesses:

Success stories abound, from small online retailers who have expanded their market reach to multinational corporations that have streamlined their payment processes in the Philippines. These narratives underscore Dragonpay's role in enabling businesses to flourish in the Philippine digital marketplace.

For businesses seeking to leverage Dragonpay for cross-border sales, understanding the transaction process is crucial. Here's a breakdown of how Dragonpay works in conjunction with a payment gateway like Tazapay to enable international transactions:

This streamlined process simplifies the complexity of international payments, making it easier for sellers to access the Philippine market without navigating the intricacies of local banking and payment systems. By leveraging the capabilities of Dragonpay through a comprehensive payment gateway like Tazapay, businesses can ensure a smooth, secure, and efficient transaction process for both themselves and their customers.

Integrating Dragonpay as a payment option for your business requires partnering with a comprehensive payment gateway like Tazapay. Tazapay simplifies the process, enabling access not only to Dragonpay but also to a wide array of local payment options across more than 80 countries with a single integration. Here's how to get started:

Tazapay's dedicated support team is available to guide you through each step, from sign-up to integration, ensuring a smooth and efficient setup process. By choosing Tazapay as your payment gateway, you not only gain access to Dragonpay but also unlock the potential to expand your business reach globally, catering to a diverse customer base with localized payment options.

Cross-border sales come with their set of challenges, from navigating local payment preferences to addressing security concerns. Dragonpay is designed to mitigate these challenges by:

Providing a familiar payment interface for Filipino consumers, thus increasing conversion rates.

Offering robust fraud detection and prevention mechanisms to safeguard transactions.

Ensuring compliance with local regulations, reducing the administrative burden on merchants.

Preparing for the Future: Trends in Cross-Border E-Commerce

The landscape of cross-border e-commerce is constantly evolving. Emerging trends indicate a shift towards more personalized and secure online shopping experiences. Dragonpay stays ahead of these trends by continuously updating its platform with features that enhance user experience and security, ensuring businesses remain competitive in the dynamic Philippine e-commerce market.

Dragonpay is more than a payment gateway; it's a strategic tool for businesses aiming to capitalize on the Philippine e-commerce boom. Its comprehensive suite of services not only facilitates access to this lucrative market but also positions businesses for success in the global e-commerce arena.